The Interest Rate Rollercoaster: How High Will They Go?

Interest rates are a fundamental element of financial systems, exerting considerable influence on everything from consumer borrowing to global economic policy. They reflect the cost of borrowing money or the reward for saving it, serving as a key mechanism for central banks to control economic activity and maintain stability. Central banks use interest rates to adjust the pace of economic growth, influence inflation, and steer economic expectations. By raising or lowering interest rates, these institutions aim to either stimulate spending and investment or cool down an overheating economy, often with far-reaching effects on household finances, business decisions, and government budgets.

The impact of interest rates on everyday life is undeniable. They shape everything from mortgage rates to credit card costs, directly influencing consumers' financial well-being. For instance, when central banks raise interest rates, borrowing becomes more expensive, which typically slows down consumer spending and business investment. Conversely, when rates are lowered, borrowing becomes more affordable, potentially stimulating demand and economic activity.

In the wake of the COVID-19 pandemic, the world has witnessed an unprecedented interest rate rollercoaster. Central banks, first caught off guard by surging inflation, responded with aggressive rate hikes to cool down overheating economies. Inflation, driven by supply chain disruptions, energy price shocks, and labor shortages, reached levels not seen in decades (International Monetary Fund, 2023). The consequences of these policies have been profound: stock markets fluctuated wildly, borrowing costs soared, and economic growth slowed.

Now, as inflation shows signs of easing, central banks face a difficult balancing act. The Bank of England has recently reduced its base rate from 4.75% to 4.5%, the lowest level in 18 months, marking its third cut since August 2024. This move signals a "gradual and careful" approach to easing monetary policy after maintaining rates at a 16-year high of 5.25%. Meanwhile, the Fed is grappling with persistent inflationary pressures, and the ECB continues to navigate the complexities of the Eurozone's economic landscape.

At the same time, some countries, such as Switzerland and Singapore, have managed to keep inflation stable without resorting to extreme rate hikes. Their strategies, which include exchange rate management and fiscal policy interventions, raise an important question: “Could alternative approaches to inflation control prevent the sharp economic downturns associated with aggressive interest rate adjustments?”

The road ahead remains uncertain. Predictions on the direction of interest rates are volatile, with central banks like the BoE indicating that further cuts are possible if inflation stabilizes. The Fed and ECB are also under pressure to strike a balance between controlling inflation and avoiding a sharp economic downturn. The key question is: “How much higher will rates go, and how long will they remain elevated?”

Another critical issue is why many Western central banks got their inflation forecasts so wrong in the first place. Early in the pandemic recovery, most central banks underestimated the scale and duration of the inflationary surge, expecting it to be temporary. This misjudgment has led to a delayed and sometimes overly aggressive response, which has raised concerns about the economic side effects of such policies. As we look ahead, central banks are likely to face even more complex challenges in navigating inflation, economic growth, and financial stability in a rapidly changing global environment.

In this blog post, we will delve deeper into the current landscape of interest rates, the next steps for the Fed, ECB, and Bank of England. The questions of how high interest rates will go, and for how long they will remain elevated, are central to understanding the future trajectory of the global economy. For those looking to explore these questions in more depth, econometric tools such as Stata provide invaluable resources for modelling interest rate dynamics, inflation trends, and central bank policy impacts. Timberlake Consultants offers access to Stata and other cutting-edge economic software, enabling researchers and policymakers to conduct robust empirical analysis in an ever-changing economic landscape.

Contents

- The Relationship Between Central Banks and Inflation: Trust, Expectations, and Policy Effectiveness

- How Inflation Expectations Shape Household Behaviour

- Central Banks at a Crossroads: Balancing Inflation, Growth, and Policy Uncertainty

- Inflation Trends and Policy Responses: The U.S. vs. the Eurozone

- The Central Bank Response: Diverging Paths

- The Road Ahead: A Delicate Balancing Act

- Conclusion

The Relationship Between Central Banks and Inflation: Trust, Expectations, and Policy Effectiveness

Inflation management has always been a core function of central banks, with monetary policy decisions shaping economic expectations and financial stability. Traditionally, central banks have relied heavily on financial market indicators and professional forecasts to assess inflation expectations. However, recent research suggests that consumer beliefs and expectations play an increasingly significant role in monetary policy effectiveness (Bernanke, 2013; Blinder et al., 2008). This shift reflects a broader understanding that the public’s perception of inflation directly influences household financial behavior, spending patterns, and wage negotiations.

One of the most critical factors in anchoring inflation expectations is public trust in central banks. When households and businesses have confidence that a central bank will effectively manage inflation, they are less likely to react strongly to short-term price fluctuations. For example, a prominent level of trust in the European Central Bank (ECB) to maintain inflation close to its 2% target helps stabilize long-term inflation expectations. If the public believes that inflation deviations are temporary, they are less likely to alter their spending and saving habits in response to short-term price increases or decreases. Research by Christelis et al. (2020) suggests that investing in institutional credibility enhances the effectiveness of monetary policy. High trust in a central bank not only lowers inflation expectations but also reduces the likelihood of precautionary savings, fostering more stable consumption patterns and investment behavior.

How Inflation Expectations Shape Household Behaviour

Empirical studies highlight the profound effect of inflation expectations on household financial decisions. Malmendier and Nagel (2016) show that households anticipating higher inflation are less inclined to invest in long-term bonds, favoring fixed-rate mortgages to hedge against potential interest rate increases. Similarly, Armantier et al. (2015) find that individuals' inflation expectations influence their investment decisions in predictable ways, aligning with economic theory. D’Acunto et al. (2016) further demonstrate that when inflation expectations rise, households exhibit a greater urgency to purchase durable goods before prices increase further. These behavioral patterns underscore the critical role of inflation expectations in shaping aggregate demand and economic stability.

Given this evidence, modern central banks increasingly use communication strategies as a key tool for anchoring inflation expectations. Transparent guidance on future monetary policy, known as forward guidance, helps prevent inflation expectations from deviating too far from the target rate. Blinder et al. (2017) argues that enhanced communication and new policy instruments, such as asset purchases and yield curve control, will remain permanent fixtures in central banking. By ensuring that inflation expectations remain well-anchored, central banks can mitigate the risk of self-fulfilling inflation spirals or economic stagnation due to deflationary fears.

Central Banks at a Crossroads: Balancing Inflation, Growth, and Policy Uncertainty

As of early 2025, central banks in the U.S., U.K., and Eurozone are at a critical juncture. After aggressively raising interest rates to combat post-pandemic inflation—fueled by supply chain disruptions, energy shocks, and labor market imbalances—these institutions now face a pivotal decision: maintain restrictive policies to solidify inflation control or begin easing rates to support economic growth (IMF, 2024; BIS, 2024). Striking this balance is proving difficult, as inflationary pressures persist in some sectors, while economic activity in others shows signs of strain.

Inflation Trends and Policy Responses: The U.S. vs. the Eurozone

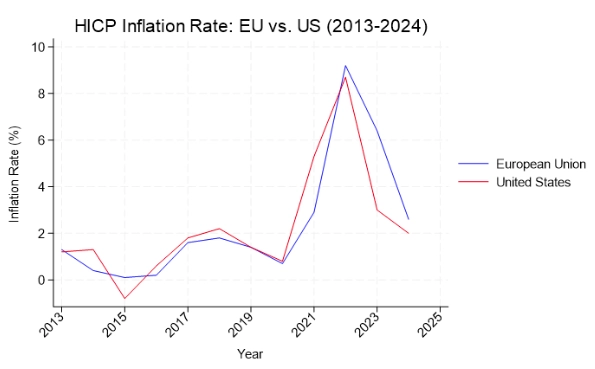

Figure 1: HICP Inflation Rate in the European Union (27 countries from 2020) and the United States (2013–2024). The Harmonised Index of Consumer Prices (HICP) is used for inflation monitoring in the EU, while the U.S. inflation rate is based on national consumer price indices. Data sourced from Eurostat.

An analysis of Harmonized Index of Consumer Prices (HICP) inflation trends in the European Union (EU-27) and the United States from 2013 to 2024 reveals distinct phases, shaped by economic shocks and policy responses. From 2013 to 2019, inflation remained stable in both regions, fluctuating around 1–2% with minor variations. However, the landscape shifted dramatically from 2021 onwards, as the global economy grappled with the aftershocks of the COVID-19 pandemic. Supply chain constraints, surging energy costs, and labor shortages drove inflation to unprecedented levels.

The inflation surge peaked in 2022, reaching 9.2% in the EU and 8.7% in the U.S., as post-pandemic recovery efforts, expansionary fiscal policies, and geopolitical turmoil—particularly Russia’s invasion of Ukraine—exacerbated cost pressures. By early 2023, disinflation began to take hold, but at varying speeds. The Eurozone’s inflation trajectory (6.4% in 2023 and 2.6% in 2024) reflects a more volatile path compared to the U.S. (3.0% in 2023 and 2.0% in 2024), where inflation moderated more steadily. Notably, by February 2022, just as Russia’s invasion began, inflation had already surged to 6.2% in the U.K., 5.2% in Germany, and 7.9% in the U.S.

This divergence raises pressing policy questions. The Fed and the ECB must carefully weigh inflation risks against economic slowdown concerns. While the rapid disinflation in both economies suggest room for interest rate cuts in 2025, the decision remains fraught with uncertainty—especially amid global trade tensions, wage growth concerns, and evolving geopolitical risks. Understanding these dynamics is essential for anticipating the next steps in monetary policy and their broader economic implications.

The Central Bank Response: Diverging Paths

The Bank of England has already pivoted toward easing, cutting its policy rate to 4.5% in February 2025, after maintaining a 16-year high for months. Similarly, the ECB has begun lowering rates, reducing its benchmark deposit rate to 2.5%, following a peak of 4%, a response to the record-high 10.6% inflation in 2022 (ECB, 2025). However, the Fed remains more cautious. With core inflation still above its 2% target and a resilient U.S. labor market, policymakers have signaled a slower approach to rate reductions (Federal Reserve, 2025).

One of the key concerns is the persistence of inflation, particularly in services and wages, which remain elevated despite the broader decline in headline inflation. This raises the risk that inflation expectations could become unanchored, forcing central banks to maintain higher rates for longer than markets anticipate (Christelis et al., 2020). Meanwhile, the Eurozone economy remains fragile, with zero growth in late 2024 and looming threats such as potential U.S. trade tariffs under President Trump, which could further dampen European exports and investment (Barclays, 2025).

The Road Ahead: A Delicate Balancing Act

Central banks now face conflicting pressures: on one hand, slowing growth calls for rate cuts, while on the other, inflationary risks—driven by fiscal expansion and geopolitical uncertainty—demand a more measured approach. Markets are searching for clear guidance, but policymakers must tread carefully to avoid financial instability.

Moreover, public trust in central banks is at stake. After underestimating inflation risks early in the post-pandemic recovery, central banks must now convince households, businesses, and investors that they can navigate inflation control without triggering a recession. The effectiveness of forward guidance, transparent communication, and credible policymaking will be critical in shaping economic expectations and ensuring monetary policy remains a stabilizing force rather than a source of uncertainty (Blinder et al., 2017).

The coming months will be pivotal. Will central banks successfully engineer a soft landing, or will prolonged monetary tightening push economies into deeper slowdowns? As global economic conditions evolve, policymakers will need to remain adaptable, ensuring that inflation is firmly under control without undermining economic growth.

Conclusion

Central banks are at a critical juncture, tasked with navigating the delicate balance between controlling inflation and supporting economic growth. Their decisions on interest rates will have far-reaching implications for consumers, businesses, and global financial stability. While their traditional tools remain essential, the current landscape of post-pandemic inflation presents new challenges—challenges that central banks are still grappling with after underestimating the persistence and scale of inflation in the early recovery period.

As we look to the future, it remains uncertain whether current monetary policies have struck the right balance. With inflationary pressures still lingering in key sectors and global uncertainties continuing to evolve, central banks will need to remain vigilant. Transparent communication, forward guidance, and the restoration of public trust will be vital for managing expectations and ensuring that policy actions are seen as credible. As policymakers face the dual pressures of tightening monetary policy to control inflation while supporting economic growth, the path forward will require flexibility and adaptability. The next few months could determine whether central banks can orchestrate a "soft landing" or if the global economy will face the consequences of prolonged uncertainty.

For economists, policymakers, and researchers seeking to navigate this complex landscape, econometric tools such as Stata offer invaluable resources for modelling interest rate dynamics, inflation trends, and central bank policy impacts. Timberlake Consultants provides access to Stata and other cutting-edge economic software, enabling in-depth analysis of economic variables in real-time. By harnessing these tools, analysts can better understand the underlying forces driving central bank decisions and provide clearer insights into how these policies will shape the future economic trajectory. As we continue to monitor the evolving situation, the question remains: “How much higher will rates go, and for how long?” The answers to these questions will not only define the next phase of global monetary policy but also influence the broader economic environment for years to come.

Francisca Carvalho, Lancaster University

Francisca is a third-year PhD student in Economics at Lancaster University. Her research focuses on climate risk factors and their impact on portfolio returns. She also teaches mathematics, econometrics, macroeconomics and microeconomics, to undergraduate and postgraduate students.

- Bank for International Settlements (BIS). (2024). Annual Economic Report.

- Barclays. (2025). Global Market Outlook.

- Bernanke, B. (2013). Communication and monetary policy. Speech delivered at the National Economists Club Annual Dinner, Washington DC. https://www.federalreserve.gov/newsevents/speech/bernanke20131119a.pdf

- Blinder, A., Ehrmann, M., Fratzscher, M., de Haan, J., & Jansen, D. (2008). Central bank communication and monetary policy: A survey of theory and evidence. Journal of Economic Literature, 46(4), 910–945.

- Blinder, A., Ehrmann, M., de Haan, J., & Jansen, D. (2017). Necessity as the mother of invention: Monetary policy after the crisis. Economic Policy, 32(92), 707-755.

- Christelis, D., Georgarakos, D., Jappelli, T., & Van Rooij, M. (2020). Trust in the central bank and inflation expectations (No. 2375). ECB Working Paper.

- D'Acunto, F., Hoang, D., & Weber, M. (2016). Unconventional fiscal policy, inflation expectations, and consumption expenditure. CESIFO Working Paper, 5793.

- Eurostat. (n.d.). Harmonised indices of consumer prices (HICP) – annual data (average index and rate of change). European Commission. Retrieved from https://ec.europa.eu/eurostat/databrowser/view/PRC_HICP_AIND/default/table?lang=en

Related Posts

-

More

-

More

MoreIs the World Heading for a Soft Landing in 2026?

-

More

MoreA Generation at Risk: The Realities of Youth Unemployment in Europe and the UK

-

More

MoreRebuilding Economies After Natural Disasters: What Does The Data Say?

-

More

MoreAI’s Hidden Cost: The Unanswered Question of Energy Consumption

-

Cambridge 2025More

Cambridge 2025MoreCausal Machine Learning: Principled Approaches for Econometric Analysis